After dropping the benchmark federal funds rate to a range of 0%–0.25% early in the pandemic, the Federal Open Market Committee of the Federal Reserve has begun raising the rate aggressively in response to high inflation and a stronger economy.

Following 0.25% and 0.50% increases in March and May 2022, the Committee implemented successive 0.75% increases at its June and July meetings — the first 0.75% increases since 1994 — to a target range of 2.25%–2.50%. June projections (most recent available) indicate the rate could rise to a range of 3.25%–3.5% by the end of 2022 with an additional one or two 0.25% increases in 2023.1

Rates and Bond Prices

Raising the federal funds rate places upward pressure on a wide range of interest rates, including the cost of borrowing through bond issues. When interest rates go up, the prices of existing bonds typically fall, because new bonds with higher yields are more attractive. Investors are also less willing to tie up their funds for a long time, so bonds with longer maturity dates are generally more sensitive to rate changes than shorter-dated bonds. Yet shorter-dated bonds usually have lower yields.

Despite the challenges, bonds are a mainstay for conservative investors who may prioritize the preservation of principal over returns, as well as retirees in need of a predictable income stream.

Step by Step

One way to address rising rates is to create a bond ladder, a portfolio of bonds with maturities that are spaced out at regular intervals over a certain number of years. For example, a five-year ladder might have 20% of the bonds mature each year. This strategy puts an investor's money to work systematically, without trying to predict rate changes.

With rates projected to continue rising, it might make sense to create a shorter bond ladder now and a longer ladder when rates appear to have stabilized. Keep in mind that these are only projections, based on current conditions, and may not come to pass. The actual direction of interest rates might change.

Reinvesting or Taking Withdrawals

When bonds from the lowest rung of the ladder mature, the funds are often reinvested at the long end of the ladder. When rates are rising, investors who reinvest the funds may be able to increase their cash flow by capturing higher yields on new issues. Or a ladder might be part of a withdrawal strategy in which the returned principal from maturing bonds is dedicated to retirement spending.

Bond ladders may vary in size and structure, and could include different types of bonds depending on an investor's time horizon, risk tolerance, goals, and personal preference. Owning a diversified mix of bond investments might also help cushion the effects of interest rate and credit risk in a portfolio. Diversification is a method used to help manage investment risk; it does not guarantee a profit or protect against investment loss.

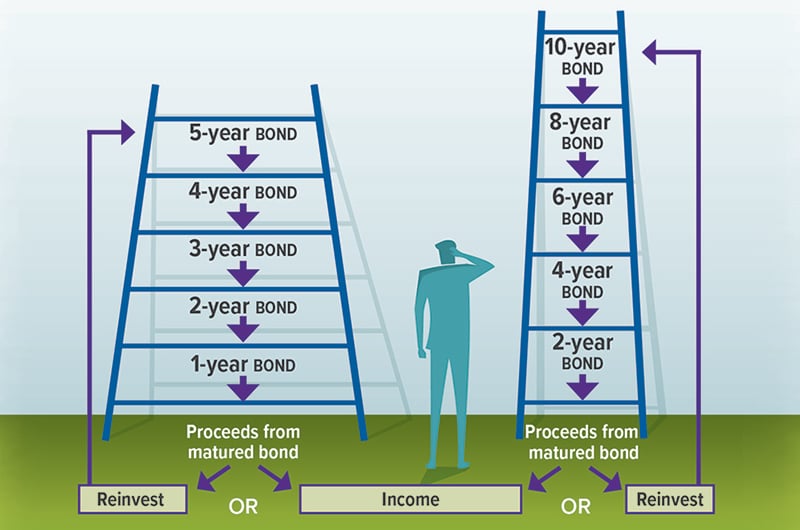

Rung by Rung

Here are two sample structures for a bond ladder. When bonds mature, the proceeds can be used for income or reinvested in bonds to fill the longest maturity rung.

Individual Bonds vs. ETFs

Buying individual bonds provides certainty, because investors know exactly how much they will earn if they hold a bond to maturity, unless the issuer defaults. However, individual bonds are typically sold in minimum denominations of $1,000 to $5,000, so creating a bond ladder with a sufficient level of diversification might require a sizable investment.

A similar approach involves laddering bond exchange-traded funds (ETFs) that have defined maturity dates. These funds, typically called target maturity ETFs, generally hold many bonds that mature in the same year the ETF will liquidate and return assets to shareholders. Target maturity ETFs may enhance diversification and provide liquidity, but unlike individual bonds, the income payments and final distribution rate are not fully predictable. Bond ETFs are subject to the same inflation, interest rate, and credit risks associated with their underlying bonds.

Exchange-traded funds are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained from your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

1) Federal Reserve, 2022

Prepared by Broadridge Advisor Solutions Copyright 2022.