The Roth IRA is a powerful tax-favored retirement option since it can offer a hedge against future tax-rate increases. But beyond tax planning considerations, Roth IRAs have several important advantages over traditional IRAs:

1. Unlike a traditional IRA, a Roth IRA distribution is tax-free if you’ve had the account open at least five years, and reached the age of 59½, become disabled or died.

2. You can make contributions to your Roth IRA after age 70½, depending on whether you fall within the earned income limits.

3. Roth IRAs are not subject to the traditional IRA rules for required minimum distributions at age 70½.

The Internal Revenue Code allows IRA owners to convert significant sums from traditional IRAs to Roth IRAs. But you have to follow these important rules (among others):

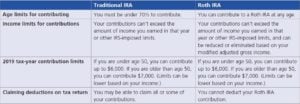

- The ability to contribute tails off at higher incomes. For 2019, the eligibility to make annual Roth IRA contributions is phased out between modified adjusted gross income (MAGI) levels of $122,000 to $137,000 (unmarried individuals) and $193,000 to $203,000 (married joint filers).1

- The conversion is treated as a taxable distribution from your traditional IRA. Doing a conversion likely will trigger a bigger federal income tax bill and possibly a larger state income tax bill. However, today’s lower federal income tax rates might be the lowest you’ll see in your lifetime, and the tax benefits of avoiding higher taxes in future years may extend to family members after death.

Many tax experts suggest that the best reason to convert some or all of your traditional IRA to a Roth IRA is if you believe your tax rate during retirement will be the same or higher than what you are paying currently. Since you’re no longer allowed to reverse a Roth IRA conversion, it’s important to understand the tax ramifications. Talk to your tax advisor before taking any action.

Traditional vs. Roth IRA: High-Level Comparison

Here is a simplified comparison of IRA rules and tax benefits. Remember, tax laws are complex and subject to change. Consult a tax advisor about your individual situation before taking action.

1Source: Bill Bischoff, “How the new tax law created a ‘perfect storm’ for Roth IRA conversions in 2019,” MarketWatch.com, Jan. 16, 2019. https://www.marketwatch.com/story/how-the-new-tax-law-creates-a-perfect-storm-for-roth-ira-conversions-2018-03-26