The inversion of the treasury yield curve is not a perfect predictor of a recession. Yet when the yield curve inverted Wednesday, with the 10-year yield falling below the 2-year yield, we witnessed the equity markets fall through the floor. The Dow fell more than 800 points and the S&P 500 lost around 3% in a single day as investors fled out of equities and into safer assets as the yield curve inversion heightened prospects that a recession was imminent.

So, what caused this inversion? And does it really mean we’re heading towards a recession?

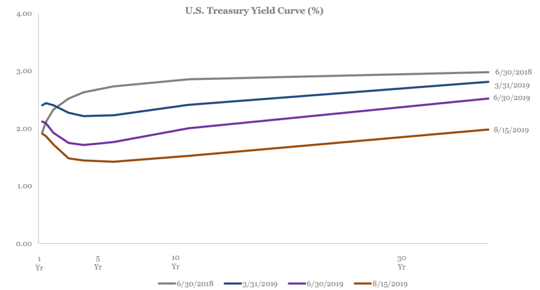

What caused the yield curve inversion?

Economic reports from both China and Germany Wednesday morning showed that both economies are showing signs of weakness. China reported several readings that came in below expectations and a jobless rate that hit its highest level since reporting of that data began. Germany announced even worse news as it reported its economy had shrunk in the second quarter.

This news comes on top of the continued escalation of trade tensions between the United States and China. Both sides have announced a ramping-up of retaliatory measures in the last few weeks, heightening concerns of a global economic slowdown.

Both events converged Wednesday and heightened, sending the 10-year yield lower than the 2-year yield as investors absorbed the possibility of an economic slowdown. This comes after several quarters of the yield curve flattening, bringing the 10-year and 2-year yield closer together.

Does this mean we’re heading towards a recession?

Market pundits for decades have touted the inversion of the yield curve as one of many predictors of a coming recession. While the inversion of the yield curve has preceded each of the seven recessions we’ve experienced since 1962, there have also been inversions that have normalized and not preceded a recession. Given that, it is important to look at the underlying factors driving the yield curve to flatten, and ultimately invert.

Over the last several years, as this economy has continued to show signs of strength, the Federal Reserve has been steadily raising short-term interest rates, driving short-term yields up with it. During that same period, long-term yields have failed to keep up the same pace as short-term yields, and the yield curve flattened as a result. The reason long term yields have remained less responsive than short term yields has been a source of great debate. For many, longer-term yields have remained anchored because of fears that our current economic expansion, now the longest in history, is coming to an end.

The other side of this debate believes it is not the expectation of lower long-term growth that has grounded long-term yields, but the supply and demand forces in the market. Global demand for long term U.S. treasuries increased significantly over the last several years as aggressive central bank policies have driven yields in multiple countries, making higher-yielding U.S. treasuries the preferred asset for risk-aware investors looking for yield. This high demand creates a dampening effect, keeping longer-term yields at bay.

So which side is right? We don’t believe in an “either-or” scenario. Certainly, there is some evidence that points to a weaker economic outlook for the United States, but to ignore the effect the demand for long term U.S. treasuries has on the yield curve would be turning a blind eye.

What is the outlook based on the yield curve inversion?

Even if this inversion does in fact signal the next recession, the U.S. probably isn’t on the precipice of it yet; looking at the last 50 years, a yield curve inversion typically preceded a recession by 12 to 24 months. It is also important not to view the yield curve inversion in isolation. There are still signs of strength for the economy including a 50-year low in the unemployment rate, steadily rising wages and strong consumer spending.

While negative economic reports are typically the ones that grab headlines, sifting through the madness can often leave you with a better picture than those headlines portray. Our economy may be far from perfect, but so is the predictability of an inversion for a recession.

In any case, an inversion of the yield curve is certainly an eye-raising event. If this event has you concerned about your portfolio and the effects a recession would have on it, now may be a good time to review your asset allocation to see if you are properly invested based on your goals and risk tolerance. As always, the Financial Wellness Help Center is here to assist you with your questions.